Secondary Offices - A Case For Investors?

What comes next for secondary offices

We’ve recently learnt that working from home is a viable alternative to the office. If we are to go to the office, it needs to be superior to what the home has to offer. This has led to a flight to quality for best-in-class offices, with secondary offices being left behind.

The decline of secondary offices is temporary, not permanent. In the long run, demand will pick up. What they offer is a place to work at a reasonable price. That being said, landlords cannot expect occupiers to magically show up. They need a game plan.

Secondary Offices - A Case For Investors?

With working from home becoming the norm for many of us, we tend to forget how the office has set the foundations for us to do so successfully. We were able to get through Covid as we had built up our networks, mentoring and training from the office. Whilst working from home would not have been possible without technology, it has not replaced the need for an office.

Many employees do not want to return to the office, but it is what they and their employers need. The office allows us to learn from our bosses, build long-term relationships and close those important deals. It is good for our productivity and our mental health. The fact most decision-makers still have an office presence says a lot. Whatever the future holds, the office is here to stay. And no, we don't all need to be in the office five days a week.

Whilst secondary offices have a future, the investment outlook is bleak. Occupiers are downsizing and there is a flight to quality office space. At the same time, rising interest rates are affecting landlords who are no longer willing or able to acquire older buildings. As a result, the office market is experiencing a shift.

Considering the harsh reality, an adjustment in pricing has to be reflected. Currently, there are not enough sellers willing to accept this. As put by Joshua Chaffin at the FT:

That’s what everyone is waiting for: this incredible revaluation.

For that to change, sellers need to lower their expectations. Eventually, some will be forced to. That is where the opportunity lies. Buyers taking a long-term view of the market beyond the short-term noise.

As landlords have discovered, occupiers do not magically show up anymore. There are viable alternatives, so if we are to come to the office, we expect minimum standards. Whilst the attention has recently been on shiny new buildings, we should not underestimate the need for ‘modernised’ secondary offices. With these, landlords would spend modest capex works, yet enough to make the building attractive at a reasonable price. The offering would be hassle-free and include modern office amenities such as wi-fi, furniture and desks, end-of-journey facilities and flexible lease terms. They’d provide collaborative spaces and the physical presence essential for so many companies to function. The key differentiator from the shiny new buildings is pricing and more modest specifications. As we enter a tougher economic climate, this might be what many companies require and can afford.

As ever, location plays a crucial part. Prime central business districts make the most sense, whilst regional up-and-coming cities should not be underestimated. Residential neighbourhoods are also of interest, with a rise in remote work making workspaces closer to home appealing. For many, the issue is not the office, it’s the commute.

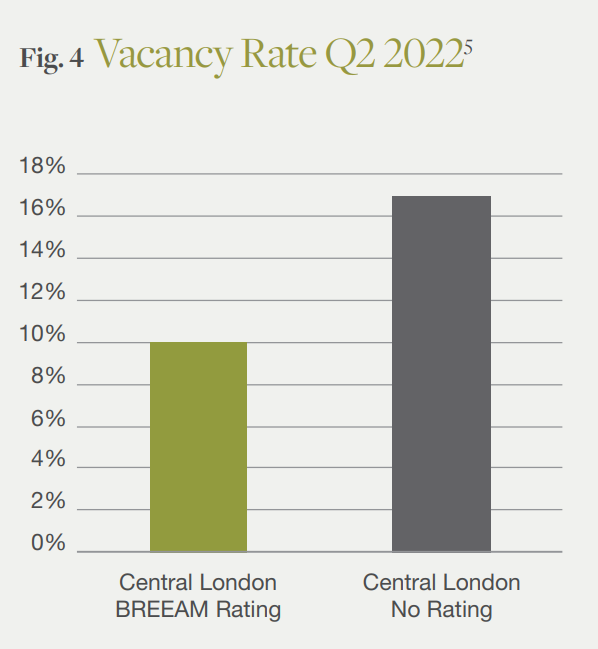

Looking at energy efficiency, Hines research has compared vacancy rates between buildings with and without a BREEAM certification, with the evidence showing lower vacancy for buildings with BREEAM Ratings (see graph below). The push has been for sustainability in Grade A offices, but this should not stop us from taking the same approach with Grade B offices. Regarding UK legislation, from April 2023 offices with EPCs of F or G will not be permitted to be occupied. Owners will be forced to make a decision. Upgrade the space, keep it vacant, or sell. There are hundreds, if not thousands of these offices in the UK. An opportunity awaits those able to spot them.

Lastly, we cannot ignore conversions. Residential makes the most sense, whilst distribution centres, data centres and even urban farms have also been considered. This is inevitable with many offices, especially those in the wrong location and where there is an oversupply. This won’t be the case with all offices as many are constrained by costs, regulations and physical challenges.

Final thoughts

It is tough out there. Demand is low whilst supply is increasing. Capex, energy and borrowing costs are all rising. No surprise yields are softening, prices are dropping and investors have little appetite. Yet this is where the opportunity lies.

Despite work from home being here to stay, so is the office. Modernised secondary buildings at a reasonable price fulfil both what employees need and what many employers can afford.

From an investment perspective, the winners will need to look beyond the short-term noise, pick the right location and have the right strategy. The risk is significant and must be reflected in the price. Whilst many vendors are unwilling to accept this, they might soon be forced to.

A couple of thoughts from the past month:

I highly recommend reading What it Takes, by Stephen Schwarzman (Blackstone co-founder). Fact: In 2006 Blackstone transacted $70 billion of real estate in 2 months. That’s equivalent to over $1 billion a day for 60 days!

A recent newsletter discovery about the great online game - Cyber Patterns

A fantastic Twitter thread on the history of mixed-use areas.