Interest Rates and UK Commercial Real Estate

Interest Rates and UK Commercial Real Estate

What rising interest rates mean for commercial real estate

A turbulent few months in the United Kingdom. A new monarch, two new prime ministers, a failed “mini” budget and an uncertain real estate market. Here I focus beyond the short-term noise and look at the longer-term implications.

One of my main reflections is that no one can predict what happens next. The months and possibly years ahead will be difficult. Tough calls will need to be made. Those making the right calls will come out the big winners.

Interest Rates and UK Commercial Real Estate

The year is 2021 and the economy is booming. Money is cheap, the stock market is in the green and real estate prices are on the rise. We know the party will eventually end, yet we do not want to accept it. Come 2022, and the party is well and truly over. Cheap (free) money is a thing of the past, stock markets are in the red and property values are in decline.

One of the main factors contributing to this is rising interest rates. Over the past 10+ years, we have become accustomed to cheap money and interest rates being close to 0%. With surging inflation, central banks have been left with little choice but to increase rates and control inflation. This means the end of an era of cheap money. As put by Scott Singer at Avison Young:

Living through a decade when the base rate was close to zero has warped our perception of what ‘normal’ rates are.” If you average the Federal Funds Rate (US) out since 1971 it comes in at around 5.4 percent. The rate has even gone as high as 14.6 percent in 1980.

So what does this mean for real estate? Two significant impacts are the cost of borrowing and a rise in government bond yields. Rising interest rates mean a rise in borrowing costs and government bond yields. More on this here and here.

Investors are worried if property income can cover their cost of borrowing and are considering investing in government bonds instead of real estate (offering similar returns).

This uncertainty has made investors nervy. It has put transactions on hold, renegotiated and called off. Not all owners want to sell, yet most buyers want a discount. Even where there is no discount, the perception of the market is that all assets should be trading at a discount. A lack of transactions has made valuing properties hard in today’s market. As put by Stifel analyst, Alan Carter:

For the first time since 2008, I have sympathy for valuers. Trying to establish the scale of negative yield movement has now become a pointless exercise. Instead, it’s more of a finger-in-the-air guess as to whether yields rise by anywhere between 50bps and 300bps, the former of which would be containable, the latter catastrophic. Neither I nor anyone else has a clue on that outcome at present.

The market is uncertain and what is needed more than anything is stability. An excellent summary put by Ezra Nahome, CEO of LSH:

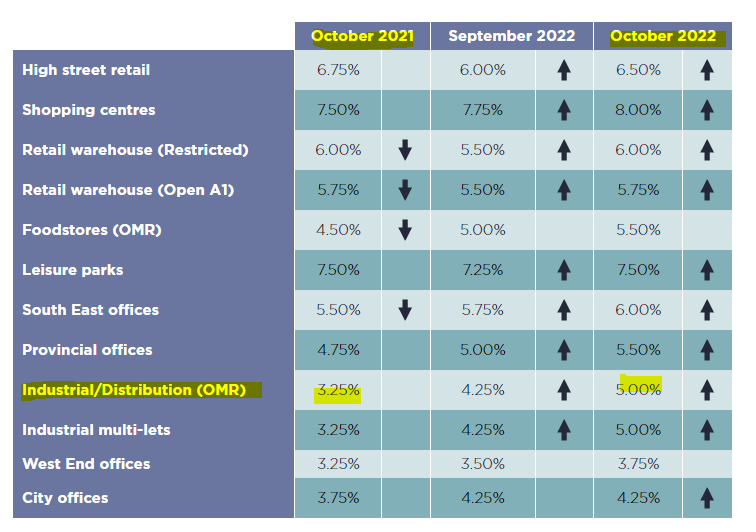

The long era of ultra-low interest rates and cheap finance has come to an end, ushering in a paradigm shift in the market. Yields have already moved out across the board, with some sectors being hit harder than others.

“While a correction is underway, uncertainty over its duration and severity is giving rise to indecision and delay. This is likely to be reflected in another subdued quarter in Q4, after which greater clarity around the economy and interest rates should hopefully emerge in 2023, providing much-needed stability and a return to transactional activity.

Whether it be debt obligations, refinancing, liquidating assets, or needing cash, owners are selling. This is where opportunistic buyers come into play, especially cash buyers. They are buying at a discount to long-term values, they do not worry about borrowing costs and are likely to receive better terms as cash buyers. The UK real estate market is even more appealing to foreign investors, specifically US investors. On top of the c. 20% discount they can achieve on assets (some assets at 0% discount, some at 40%!), they can add another c. 20% on the back of a strong $USD.

Buyers vary from high-yielding assets such as retail to low-yielding assets such as prime offices.

Retail. An unloved sector for so long. Nonetheless, the sector is still around and looking at a comeback. No doubt about a decreasing demand, whether from an occupational or an investment perspective. With yields having drifted so far out, investors remain optimistic and are spotting opportunities. High risks remain and investors must be savvy. They must be educated on the micro-location, the local economy, footfall numbers and most importantly yields, capital & rental values.

Logistics. The booming sector of recent years. Yields have compressed so far out (as low as 3%) they were bound a correction. In today’s market, there are few buyers at 3%, leaving little choice for those needing to sell but to reprice. This provides opportunities for buyers who were previously priced out. Data from Savills suggests pricing and yields are already starting to drift.

Offices. With fewer buyers at 3-3.5%, prices for offices are also softening. Buyers can consider London “trophy assets” which might have otherwise never been available to them. Whilst the discounts are out there, they are not in huge numbers.

It is another story for second-hand offices. Vacancy rates are high whilst the occupational story is weak. This provides an opportunity to buy at a discount and take on the capex works. Alternatively, investors could look at angles to repurpose the space, specifically to residential.

Alternatives. Considered to be counter-cyclical and to perform well in a downturn. These include nurseries, old age homes, and co-living. Children need to go to school, the elders need to be looked after, whilst young professionals need to go to work (or at least be out looking for work). This is regardless of the state of the economy. The counterargument is that if the economy gets that bad, people will home school, look after their parents themselves, with youngsters moving back home. Let’s hope the economy does not reach such a low.

Life sciences is another alternative sector to keep an eye on. Lab work cannot be done from home, whilst investment within the sector is increasing and supply is outstripping demand.

Energy efficiency. Regardless of asset class, energy efficiency will play a key role going into 2023 (April 2023!). Soon we will find out to what extent.

Final thoughts

Unprecedented and scary times ahead? Yes. Exciting times ahead? Also yes. Downturns have many negatives, there is no doubt. They also present opportunities. It takes the bad players out of the market and enables young and entrepreneurial players to enter the market.

In the economic climate we are in today, real estate has become as much about the vendor as about the asset. Now more than ever buyers have a shot at attractive properties at attractive prices. The key is finding the right vendor.

A couple of thoughts from the past month:

An amazing discovery is this A.I. image generation tool DALL-E. Type a sentence and DALL-E generates the art. I’ve done it with the cover of this blog post.

Big congrats to Saul Zulman on the launch of his new venture “Drop-In”. The mission is to build an ecosystem for remote workers where people can join a community, escape isolation, and work in a productive environment.

Amazing stats about one of the most famous Metaverse’s, Decentraland. Valued at $1.2 billion, this report suggests the platform only has 38 daily active users.