Offices: What Next?

Offices: What Next?

The picture is bleak. But it is not all doom and gloom.

The year is 2020. Offices are considered the safest (commercial) real estate investment asset class. Fast forward three years and this is a historical view.

Covid has come and gone, yet remote work has endured. Offices are in oversupply, whilst rising inflation and construction costs have not helped the cause.

The latest and hardest blow to all real estate is rising interest rates, which deserves a post of its own.

So, what next for offices?

Offices: What Next?

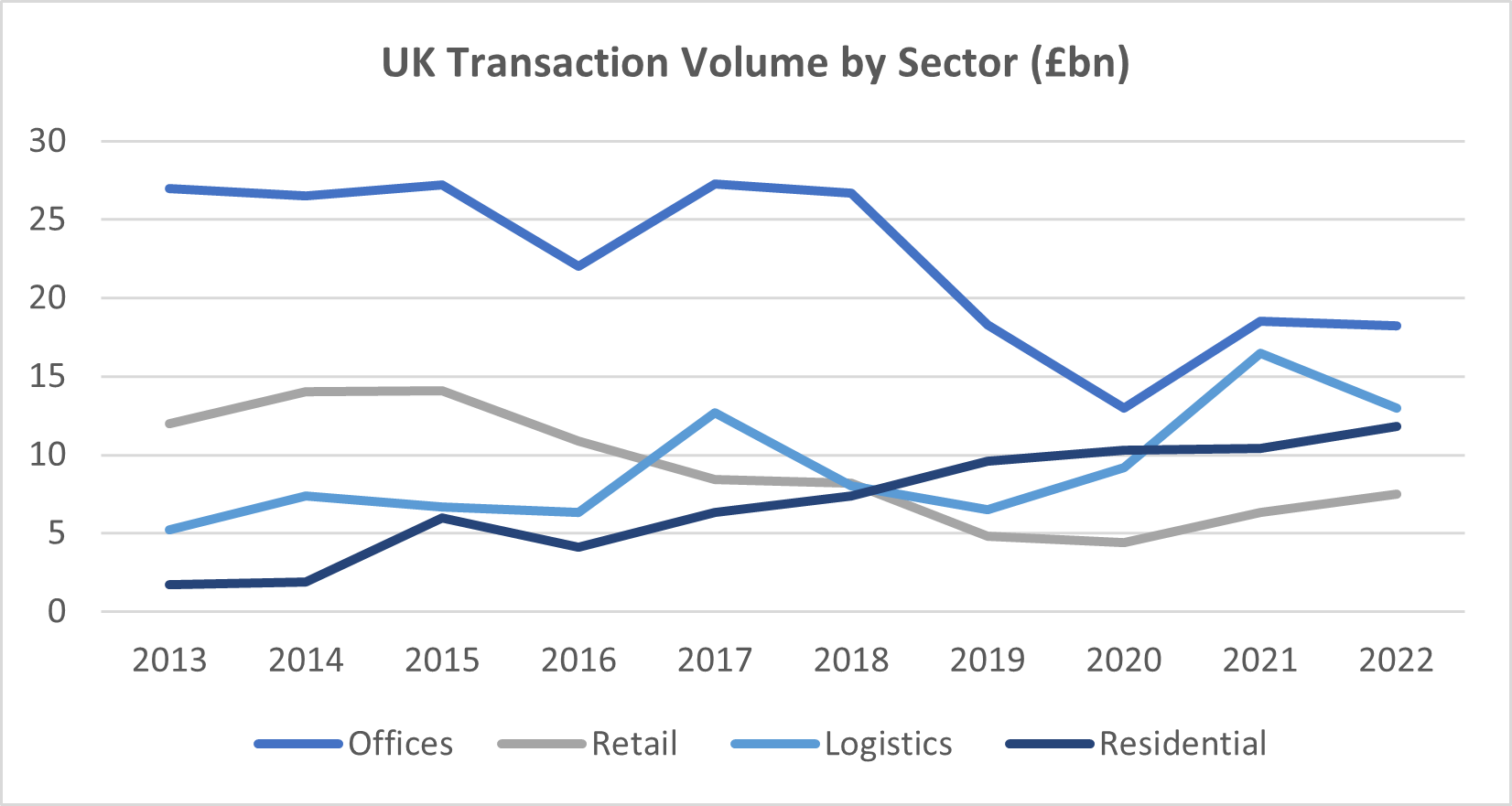

Let’s start by looking at the historical data. From 2013 to 2018, office investment transaction volumes averaged at c. £25bn a year. In the post-Covid era, this figure is averaging sub £20bn. So far in 2023 we are seeing this downward trend continue.

Source: CBRE

Yet, no matter how the office market is perceived, it still makes up for the largest (real estate) investment asset class in the UK. So is this all an overreaction? No. Logistics and residential are catching up and the question now begs how long before one of them overtakes the office.

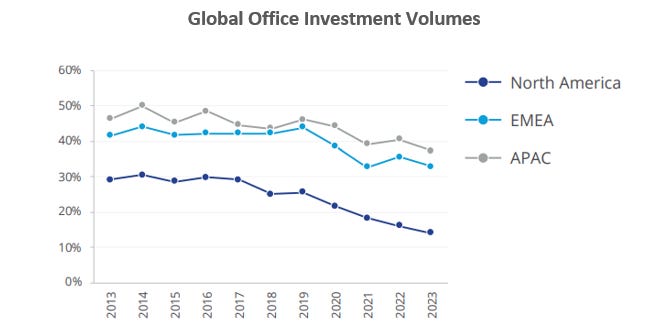

Zooming out and looking at the world’s largest market, the US, the picture is even more bleak. Whilst UK offices account for more than 30% of total transaction volumes, 15% is the figure for the US (JLL).

Sources: Colliers

Offices have been hit hard across the globe, but the graph above demonstrates how much harder the US (North America) has been hit. Why? One of the main reasons is its urban structure (I suspect there are several more reasons, but I am no expert on the US market).

Two districts within London similar to US cities are the City of London and Canary Wharf, both financial districts dominated by offices. Take away the office element and they have little else to offer. In comparison, the West End (of London) has a strong retail, leisure, and residential offering. This is regardless of the offices’ presence.

It comes as no surprise the City of London is easing its strict planning requirements that protect offices and is encouraging alternative uses. Canary Wharf is also making moves following what it has experienced with its office occupiers (ie. HSBC and others moving out. Ironically, to the City). Whilst Canary Wharf and the City are the outliers, we cannot pretend the rest of the UK office market is thriving. Investments are focused on high-end, green buildings in prime locations. Any offices not fitting these criteria are struggling with investors’ appetite.

Take for instance secondary offices. Demand is limited whilst investors expect high yields and steep discounts. That being said, as we enter challenging economic times, this might just be what office occupiers can afford. Another avenue being explored is converting offices to alternative uses such as living, storage or life sciences. In reality, this is not straightforward considering the financial implications as well as the regulatory and physical challenges. You are then left with offices with low energy efficiencies, no occupational story, and no viable alternative uses. What next for these buildings, who knows. It is also becoming common for landlords to be stuck with buildings where they do not have the know-how or financial resources to implement the necessary changes.

It is clear for all to see that the office is longer the safe investment asset class it once used to be. The market is uncertain and values have taken a hit. Investors are waiting on the sidelines or are staying away.

Yet we should not give up hope.

If we look at recent experiences from the retail sector, it is not all doom and gloom. Retail has gone through what the office is currently experiencing. People were anticipating it to be beyond recovery and investors were staying away. There was an oversupply and leases were over-rented. Many were forced to sell at a discount whilst the smart money hunted for bargains. Fast forward to today and retail has found its feet again. Rents have been rebased, yields have balanced out, and investment volumes are on the up. The office market is bound to go through a similar trajectory.

With real estate now competing with the bond market, anyone buying offices, whether prime or secondary, is expecting this to be reflected in the price. Investors focusing on the long-term fundamentals rather than the short-term noise will be the big winners. They are buying properties at a discount and are unlocking values where others are not. Lewis & Partners are here to help them find those deals.

A couple of thoughts from the past month:

Great video about the urban design of London. The city has been around since BC. Take your view on London, I suspect it is here to stay.

No doubt we will see more controversies surrounding the costs of the green transition. We need to focus more on the actual health, financial, and energy benefits of going green rather than obsessing on the green propaganda machine.

Sticking with climate, I recommend the Last Week in Climate-Tech newsletter. A weekly summary of the European Climate Tech ecosystem.