Researching UK Real Estate Investment Yields

Researching UK Real Estate Investment Yields

UK Real Estate Investment Yields. A subject I am intrigued by and often the topic of conversation. Too often do I read and talk yields, but rarely do I research and analyse them. This is the aim of this post.

Here I research UK real estate yields, analyse historical data and look at market commentary for the months and years ahead. With this, I hope to better understand how the market determines yields.

Researching UK Real Estate Investment Yields

Real Estate Investment Yields

Yields play a fundamental part in real estate. They help investors recognise risk/return, better understand the different sub-sectors and determine what price to pay for an asset. For those less familiar, let’s start by defining yields:

Yield is an indicator for the expected return of a property investment and is calculated as the ratio of rental income and the property value.

Yield = Annual Rent / Property Value

For instance, you buy a property for £1,000,000 and in return receive a yearly income of £50,000. The yield of that property is 5% (£50,000/£1,000,000=5%). The higher the yield, the higher the rental income and risk. A lower yield means a safer, lower risk investment. Factors influencing yield movement include property price, location, lease length, tenant covenant, building sustainability, inflation, etc. There are different types of yields including net initial, equivalent and prime yields. For this article, I will be focusing on prime yields, which are defined as fully rented properties of the best quality, location and tenant. To read more about yields see here and here.

Interpreting Historical Data (2016-2022)

The data below has been gathered from the Knight Frank Research on UK Investment Yields Report. The dataset is from January 2016 to April 2022 and includes several sub-sectors. For this article, I focus on:

Prime Retail

Shopping Centres

Open A1 (retail parks / essential retailers)

West End Offices

Prime Warehouses (20 years income)

Healthcare (30 years income)

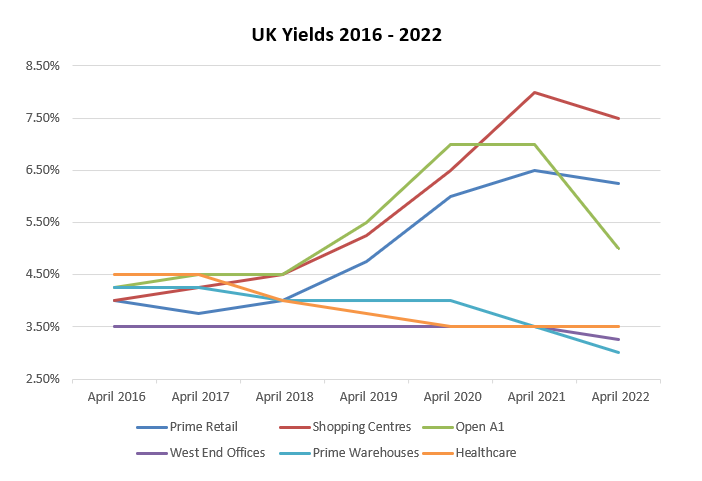

Having consolidated the data, the graph below outputs yields over the past six years:

From 2016 to 2018, yields have remained relatively stable across the sub-sectors. Since 2018 the sub-sectors have taken different directions, accelerated by Covid in March 2020.

Prime Retail, Shopping Centres and Open A1 negatively affected, becoming riskier, less attractive investments leading to yields softening. This is a result of the rise of e-commerce and the loss of appeal for shopping centres.

Open A1 experienced a recovery in 2021. Investors appreciate the importance of the sector for consumers and businesses. For instance, consumers need to shop at wholesale supermarkets/bulk buys regardless of the state of the economy.

Warehouses have been in high demand with the rise of e-commerce, exponentially increased by Covid. Healthcare also experiencing high demand during Covid, with both sectors appealing to investors. As a result, prices have risen and yields compressing.

Prime West End Offices experiencing limited movement with yields stable throughout the past six years. Some scares for the office market at the height of Covid but this not having much of an impact on investment yields in the long run.

Before moving on to the market outlook, it is worth mentioning the JLL UK Real Estate Capital Markets Report. Their data unsurprisingly correlates with the yield movements and data used above. For instance, much higher investment demand for industrial in 2021 versus the 10-year average, with the opposite for retail.

That’s it for the historical data. For those interested in taking the data further, I have included my excel workbook below:

Market Outlook

Below is a summarised commentary from market reports which include forecasts for the months and years ahead.

Investor demand for prime Shopping Centres could rise with opportunities to emerge at discounted prices. This would result in a hardening of yields.

Aggressive bidding in the logistics/warehouse sector to continue with yields further compressing and demand expected to remain. The sector of choice throughout Covid, driving prices up and pushing yields to historic lows.

Return of positive sentiment for the retail sector with yields expected to compress. Following capital value declines across the sector, attractive pricing could lead investors back at discounted prices. This could especially be the case for out of town retail.

But, the risk of retail and logistics negatively affected by the possibility of a recession and subsequent decline in disposable income.

Yields for West End offices are at a record low (3.25%), yet remain higher than its peers in Europe, including Germany (2.55%), France (2.6%), Netherlands (3%), and Italy (3%). Generally, offices are seen as an attractive low risk investment in times of recession.

Evaluating the forecasts, one should not consider these a foregone conclusion. Some of the commentaries are contradictory, which is a good thing, suggesting not everyone agrees. Forecasts should serve as guidelines and ultimately it is up to investors and advisors to make up their own decisions.

For further research, here are a couple of the market reports I have used:

Final Thoughts

Covid has had a significant impact on real estate and has accelerated many trends. This includes the downfall of retail & shopping centres and the rise of e-commerce & logistics. Some will argue these trends are set to continue, whilst others expect some reverse trends. I discuss here why I am bullish on the future of retail.

Warehouses have experienced a boom and have been on an upwards trajectory for many years. Some expect this to continue, whilst others predict the bubble to pop. If we are to enter a recession, consumers are sure to spend less, leading to lowering demand for warehouse space and a surplus on the market.

Whilst many have suggested the end of the office, it is clear that it is far from dead. Prime West End offices appear to be one of the safest, most defensive real estate investments in the UK. It is another story for second hand offices.

When it comes to real estate investments, we all have our opinions and thoughts, but ultimately, it is impossible to predict the future. In the long run, market dynamics determine what happens and those with the best strategies (and luck) are likely to be the big winners.

Thanks for reading! If you enjoyed this post, please forward it to a friend and subscribe to receive posts straight to your inbox and support my work.